by Stephen Moore • The Washington Post

It was 40 years ago this month that two of President Gerald Ford’s top White House advisers, Dick Cheney and Don Rumsfeld, gathered for a steak dinner at the Two Continents restaurant in Washington with Wall Street Journal editorial writer Jude Wanniski and Arthur Laffer, former chief economist at the Office of Management and Budget. The United States was in the grip of a gut-wrenching recession, and Laffer lectured to his dinner companions that the federal government’s 70 percent marginal tax rates were an economic toll booth slowing growth to a crawl.

It was 40 years ago this month that two of President Gerald Ford’s top White House advisers, Dick Cheney and Don Rumsfeld, gathered for a steak dinner at the Two Continents restaurant in Washington with Wall Street Journal editorial writer Jude Wanniski and Arthur Laffer, former chief economist at the Office of Management and Budget. The United States was in the grip of a gut-wrenching recession, and Laffer lectured to his dinner companions that the federal government’s 70 percent marginal tax rates were an economic toll booth slowing growth to a crawl.

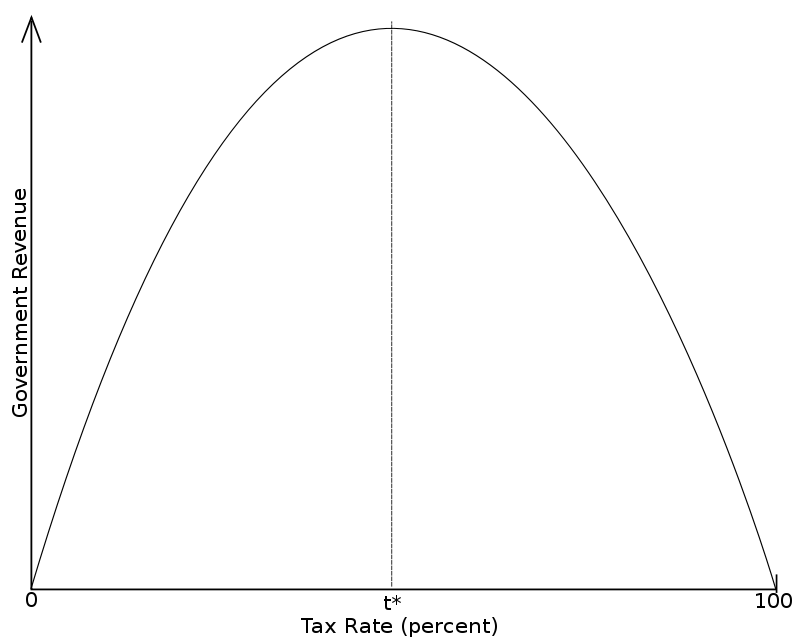

To punctuate his point, he grabbed a pen and a cloth cocktail napkin and drew a chart showing that when tax rates get too high, they penalize work and investment and can actually lead to revenue losses for the government. Four years later, that napkin became immortalized as “the Laffer Curve” in an article Wanniski wrote for the Public Interest magazine. (Wanniski would later grouse only half-jokingly that he should have called it the Wanniski Curve.)

This was the first real post-World War II intellectual challenge to the reigning orthodoxy of Keynesian economics, which preached that when the economy is growing too slowly, the government should stimulate demand for products with surges in spending. The Laffer model countered that the primary problem is rarely demand — after all, poor nations have plenty of demand — but rather the impediments, in the form of heavy taxes and regulatory burdens, to producing goods and services.

In the four decades since, the Laffer Curve and its supply-side message have taken something of a beating. They’ve been ridiculed as “trickle down” and “voodoo economics” (a phrase coined in 1980 by George H.W. Bush), and disparaged in mainstream economics texts as theories of “charlatans and cranks.” Last year, even Pope Francis criticized supply-side theories, writing that they have “never been confirmed by the facts” and rely on “a crude and naive trust in the goodness of those wielding economic power and in the sacralized workings of the prevailing economic system.” And this year, French economist Thomas Piketty penned a best-selling back-to-the-future book arguing for a return to the good old days of 70 percent tax rates on the rich.

But I’d argue — and not just because Laffer has been a longtime friend and mentor — that his theory has actually held up pretty well these past 40 years. Perhaps its critics should be called Laffer Curve deniers.

Solid supporting evidence came during the Reagan years. President Ronald Reagan adopted the Laffer Curve message, telling Americans that when 70 to 80 cents of an extra dollar earned goes to the government, it’s understandable that people wonder: Why keep working? He recalled that as an actor in Hollywood, he would stop making movies in a given year once he hit Uncle Sam’s confiscatory tax rates.

When Reagan left the White House in 1989, the highest tax rate had been slashed from 70 percent in 1981 to 28 percent. (Even liberal senators such as Ted Kennedy and Howard Metzenbaum voted for those low rates.) And contrary to the claims of voodoo, the government’s budget numbers show that tax receipts expanded from $517 billion in 1980 to $909 billion in 1988 — close to a 75 percent change (25 percent after inflation). Economist Larry Lindsey has documented from IRS data that tax collections from the rich surged much faster than that.

Reagan’s tax policy, and the slaying of double-digit inflation rates, helped launch one of the longest and strongest periods of prosperity in American history. Between 1982 and 2000, the Dow Jones industrial average would surge to 11,000 from less than 800; the nation’s net worth would quadruple, to $44 trillion from $11 trillion; and the United States would produce nearly 40 million new jobs.

Critics such as economist Paul Krugman object that rapid growth during the Reagan years was driven more by conventional Keynesian deficit spending than by reductions in tax rates. Except that 30 years later, President Obama would run deficits as a share of GDP twice as large as Reagan’s through traditional Keynesian spending programs, and the economy grew under Obama’s recovery only half as fast.

Supply-side economics was never just about slashing tax rates. As Laffer told me in a recent interview: “We also emphasized sound money, free trade and deregulation. It was a package of reforms to clear away the obstacles to increased economic output.”

I asked Laffer about the economy’s surge, while income tax rates rose, during the Clinton presidency — which critics cite as repudiation of supply-side theories. Laffer noted that tax rates on work and investment fell in the ’90s. “Under Clinton we had the biggest reduction in government spending in 30 years, one of the steepest reductions in the capital gains tax, a big cut in the tax on traded goods thanks to NAFTA, and welfare reforms which dramatically increased incentives to work. Of course the economy soared.”

As to the concern that supply-side tax-cutting has exacerbated income inequality: The real story of the 1980s and ’90s was one of upward economic mobility. After-tax incomes of middle-class families rose by roughly 30 percent (when taking into account government benefits and correctly adjusting for inflation) from 1982 to 2005. The middle class didn’t shrink, it grew richer — though the past decade has seen a big reversal.

Perhaps the most powerful vindication of the Laffer Curve comes from the many nations around the world that have successfully integrated supply-side economics into their fiscal policies. World Bank statistics reveal that almost every nation — from China to Ireland to Chile — has much lower tax rates today than in the 1970s. The average income tax rate among industrialized nations has fallen from 68 percent to less than 45 percent. The average corporate tax rate has fallen from nearly 50 percent to closer to 25 percent today. Political leaders learned from Reagan that in a globally competitive world, jobs, capital and wealth tend to migrate from high- to low-tax locations.

This vital link between low taxes and jobs has played out within the United States as well. It helps explain why, from 2002 to 2012, Texas — with no income tax — gained 1 million people in domestic migration, while almost 1.5 million more Americans left California, with its 12 percent top tax rate, than moved there.

It’s worth noting that there has been some shift in emphasis among advocates of supply-side economics. The original Laffer Curve illustrated that two tax rates lead to zero revenue: a rate of zero and a rate of 100 percent — because no one will work if all earnings are taken away. Yes, in some cases tax rates can get so high that cutting them will raise more revenue, not less. That was clearly true when capital-gains tax rates were slashed in the 1980s and 1990s, and when in 2004 the federal government enacted a repatriation tax cut on foreign earnings held captive overseas. Revenue rose in all of these instances. But today, even the most ardent disciples of the Laffer Curve don’t argue that cutting tax rates will increase revenue — except in extreme cases when rates are at the very highest range of the curve.

We do argue, and history is our guide, that lower tax rates are a private-sector stimulus that in many circumstances will rev up growth and lead to more jobs. It’s a happy byproduct that this growth will help generate higher revenue than the government’s “static” estimates always undercount.

Alas, the Laffer Curve effect is now working against the United States on corporate taxation. Our highest-in-the-world corporate tax rate of nearly 40 percent is chasing iconic U.S. companies such as Burger King and dozens of others out of the country for lower-tax climates where rates are half as high.

Even liberals unwittingly acknowledge the Laffer Curve truth when they support higher tobacco taxes to stop smoking or a new carbon tax to reduce global warming. If higher carbon taxes reduce CO2 emissions, why is it so hard to understand that higher taxes on work or investment lead to less of these?

When I asked Laffer if, 40 years later, there is any point of consensus in economics on the Laffer Curve, he replied: “I think today everyone agrees with the premise that when you tax something you get less of it, and when you tax something less, you get more of it.”

Stephen Moore is chief economist at the Heritage Foundation and a co-author with Arthur Laffer of “An Inquiry Into the Nature and Causes of the Wealth of States.”