“Despite what some argue, North American energy independence is not out of reach. The massive production gains expected in Canada combined with the output from Mexico and US domestic reserves could total 2.75 billion barrels per year by 2030. This figure exceeds expected US petroleum consumption by such a wide margin. This is only possible if increased volumes of Canadian petroleum can reach more distant US markets for competitive cost. To that end, pipeline projects such as Keystone XL are vital to any strategy of displacing oil imports from outside North America. Without them, Canadian oil will remain uncompetitive with foreign oil arriving by tanker, and even dramatic increases in Canadian production figures would not result in a reduced dependence on OPEC for most regions of the United States.”

“Despite what some argue, North American energy independence is not out of reach. The massive production gains expected in Canada combined with the output from Mexico and US domestic reserves could total 2.75 billion barrels per year by 2030. This figure exceeds expected US petroleum consumption by such a wide margin. This is only possible if increased volumes of Canadian petroleum can reach more distant US markets for competitive cost. To that end, pipeline projects such as Keystone XL are vital to any strategy of displacing oil imports from outside North America. Without them, Canadian oil will remain uncompetitive with foreign oil arriving by tanker, and even dramatic increases in Canadian production figures would not result in a reduced dependence on OPEC for most regions of the United States.”

by Kenneth Bloomquist

Executive Summary

In 2013, the United States imported 16% of the total energy it consumed from all sources, 86% of which was petroleum. Reducing these imports is therefore the primary obstacle to attaining energy independence. To achieve this by 2030, approximately 2 billion barrels of imported petroleum will need to be displaced, either on the supply side by increasing domestic production or on the demand side by reducing consumption.

On the supply side, untapped petroleum reserves in northern Alaska and the outer continental shelf (OCS) have the potential to add 752 million barrels per year to American production in 2030, or about 38% of the expected demand by that time. On the demand side, electric, natural gas, and hybrid vehicles offer the potential to reduce petroleum consumption. Unfortunately, all of these automotive variants have prohibitively high costs, and federal tax credits promoting them have been unsuccessful in affecting overall fuel efficiency improvements. Likewise, biofuel alternatives such as ethanol are immensely inefficient investments that cost Americans more at the pump and in taxes, as well as through the hidden costs of increased food prices and disruptive changes to land usage. While biofuels could contribute to energy self-sufficiency, it would be at great cost to the average taxpayer and motorist.

Unless major discoveries are made in the near future or global oil prices rise to levels that make far more expensive reserves economical, the US should not be expected to achieve petroleum self-sufficiency for many decades. Energy independence would be impossible without the imposition of onerous market-distorting federal subsidies or taxes. Given the expected increases in Canadian petroleum production over the next several decades, however, North American independence is very feasible. By 2030, imports from Canada and Mexico alone could be enough to meet all of America’s remaining energy demands, even without opening Alaska or the OCS to drilling. The availability of these imports to the US market is highly dependent on the expansion of low cost US-Canadian pipelines such as the controversial Keystone XL.

The anticipated benefits of this “independence” are debatable. Economically, increased domestic production would reduce the US trade deficit by as much as $60-75 billion per year and bolster the productivity of the American labor force, which would benefit from exposure to the practices and expertise of the petroleum industry. Increased profits by US petroleum companies and their employees would generate revenue for the federal government and stimulate the economy, though by how much is unclear. These benefits aside, the global petroleum market is so large that increased US production would do little to reduce prices at the pump. Finally, long term employment gains are expected to be modest, with many construction projects offering only temporary labor opportunities that will disappear upon completion.

The global market would also still remain vulnerable to disruptions caused by flare-ups in energy exporting regions, and the economic effects of them would still be felt by the United States regardless of where its oil came from. This means that the strategic motives for entering expensive military and political commitments in those regions will remain, though improved supply stability may insulate the US economy from sudden shocks. On the other hand, ever minor increases in US petroleum production will reduce the market share and therefore revenue streams of major oil exporters, most of which have economies disproportionally dependent on those exports.

Introduction

Since the OPEC embargo of 1973, where America’s energy comes from, how much it consumes, and how much it costs have all been recurring and divisive topics in the national dialogue. In the decades since, the global economy and the amount of energy it uses has expanded exponentially. The rising global demand for energy resources and their projected scarcity continue to make Americans and their leaders wary about the future of fossil fuels and their economic dependence upon them. Recent political episodes which have gripped the regions of the world the US has historically relied upon for energy has only compounded these concerns further, sparking numerous conversations about how the US might free itself from the need to trade with unstable and oftentimes diplomatically abrasive commercial partners.

It is in these contexts that the idea of American energy independence began and endures. Many believe that if the United States were capable of producing its own energy at home, or at least in partnership with neighboring states only (the related idea of “North American energy independence”), it could avoid becoming embroiled in many expensive political and economic affairs. Others assert that America would be free from the threat of volatile oil prices, more capable of avoiding and exiting expensive security obligations in the Middle East, and wealthier domestically as native energy resources were tapped to replace those currently imported from abroad. The objective of this paper is to provide a thorough but comprehensible review of the US energy issue which examines the feasibility of American energy independence, the requisite shifts to attain it, and the benefits Americans could expect to see should energy independence be achieved.

US Energy Consumption

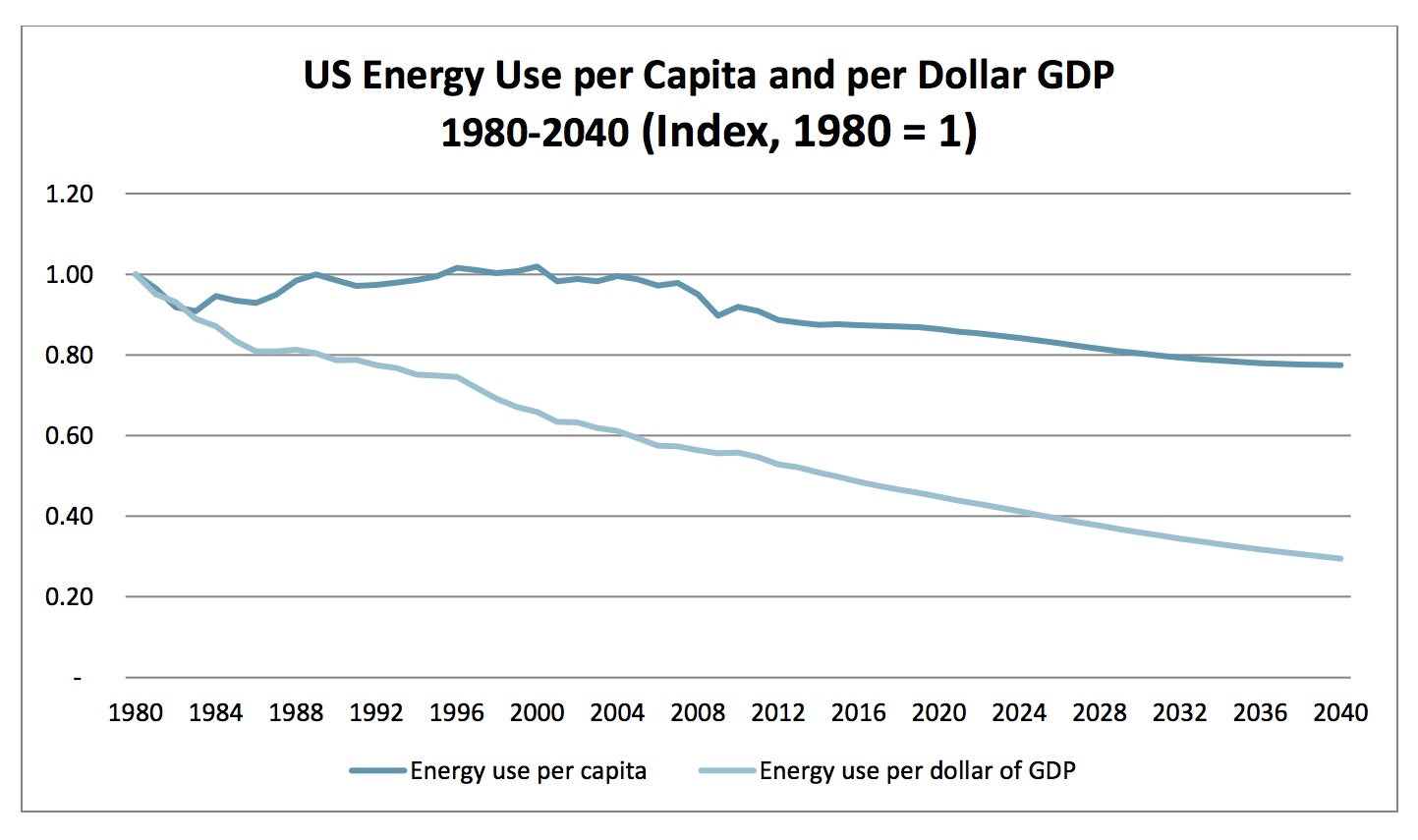

The United States was surpassed by the People’s Republic of China as the world’s leading energy consumer in 2011, consuming by most estimates about 17% of the world’s energy output compared to China’s 21% share. This shift can be attributed to the rapid economic development currently underway in Asia, with the Chinese economy growing much more dramatically than that of the United States and by extension producing and importing more energy to fuel it. By contrast, US energy consumption per capita has been declining for the past few years, due both to the lagging effects of the 2008 economic recession and increases in energy efficiency. The growing sectors of the US economy are lighter consumers of energy than those which they are replacing, leading to a sustained trend of decreasing energy use per dollar of GDP growth. Despite this, however, the average American still consumes more than three times the electricity and several more times the total energy of the average citizen of China.

This disparity in per capita energy consumption is attributed to a wide variety of factors. Americans enjoy a comparatively high amount of disposable income to spend on energy-consuming conveniences, heating, air conditioning, and cooking in their homes. The expansive geography of the country and subsequent abundance of cars and other vehicles also make the US transportation sector a tremendous consumer of petroleum, and lower gasoline prices compared to other places in the world encourage consumers to buy and use more personal transportation. Plentiful housing, diverse climates, and the highest population of any post-developed nation further multiply this consumption to a staggering total.

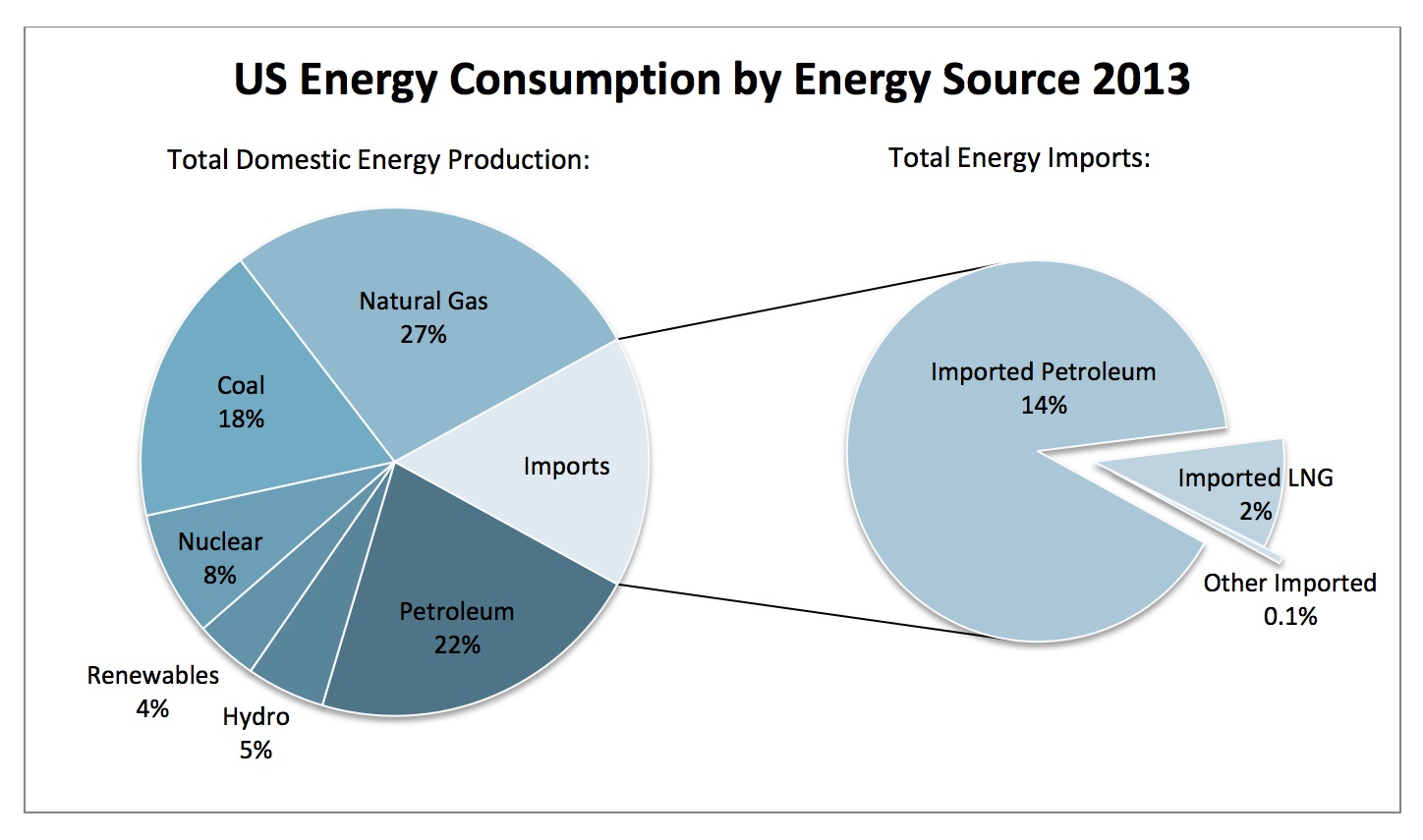

The energy Americans consume comes from six primary sources: petroleum, natural gas, coal, nuclear fission, hydroelectric, and other renewable energy sources such as solar, wind, tidal, and biomass (placed in the same category for simplicity of comparison). Despite its immense demand for power, the US’ own plentiful reserves of these fuel resources allow it to produce over 84%of its energy domestically. The remaining 16% balance is imported, overwhelmingly in the form of crude oil and other petroleum products from all parts of the world.

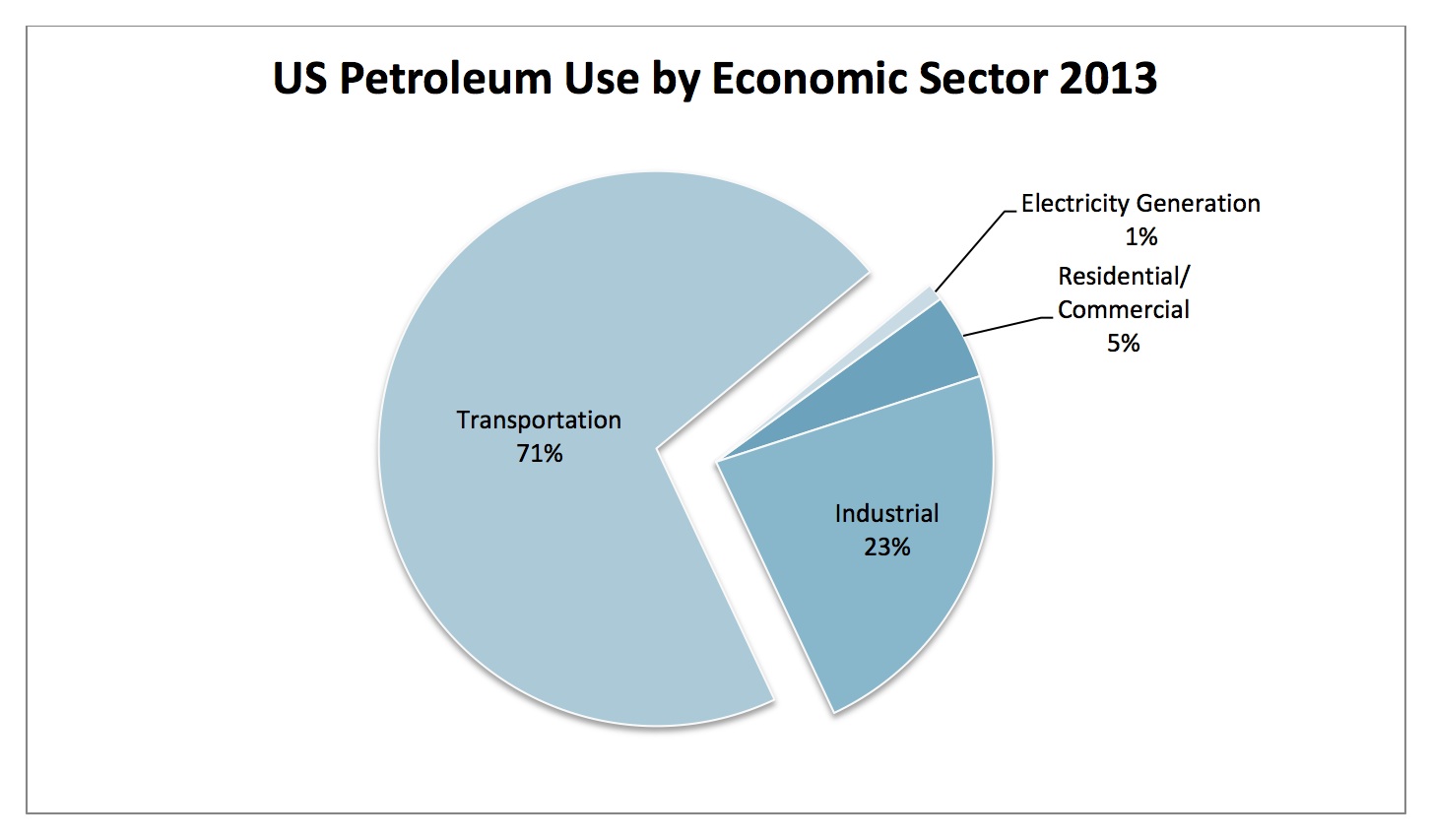

Energy from these six sources is divided between and consumed by four primary sectors of the American economy: residential/commercial (households and service industry), industrial (manufacturing), transportation, and electricity generation. For the past few decades, average American energy use per household has remained largely unchanged as increases in demand for energy consuming conveniences have been countered by increased efficiency. The same is true of the transportation sector, with the effects of a growing number of gasoline-consuming vehicles being mitigated by newer, more efficient vehicles that are making up larger shares of the US automotive fleet. Most growth in energy use comes from the industrial sector of the economy, especially as attractive domestic natural gas prices have stimulated a number of domestic industries.

Dependence on Foreign Petroleum

Petroleum accounts for 36% of American energy consumption, the largest share of any energy resource. Additionally, the US petroleum deficit is the largest of any energy source, meaning that the amount of petroleum Americans use significantly outstrips the amount of it produced within their borders. About one third of all petroleum Americans use must be imported from abroad to make up this difference in petroleum produced and consumed, representing about 14% of all energy the US uses annually.

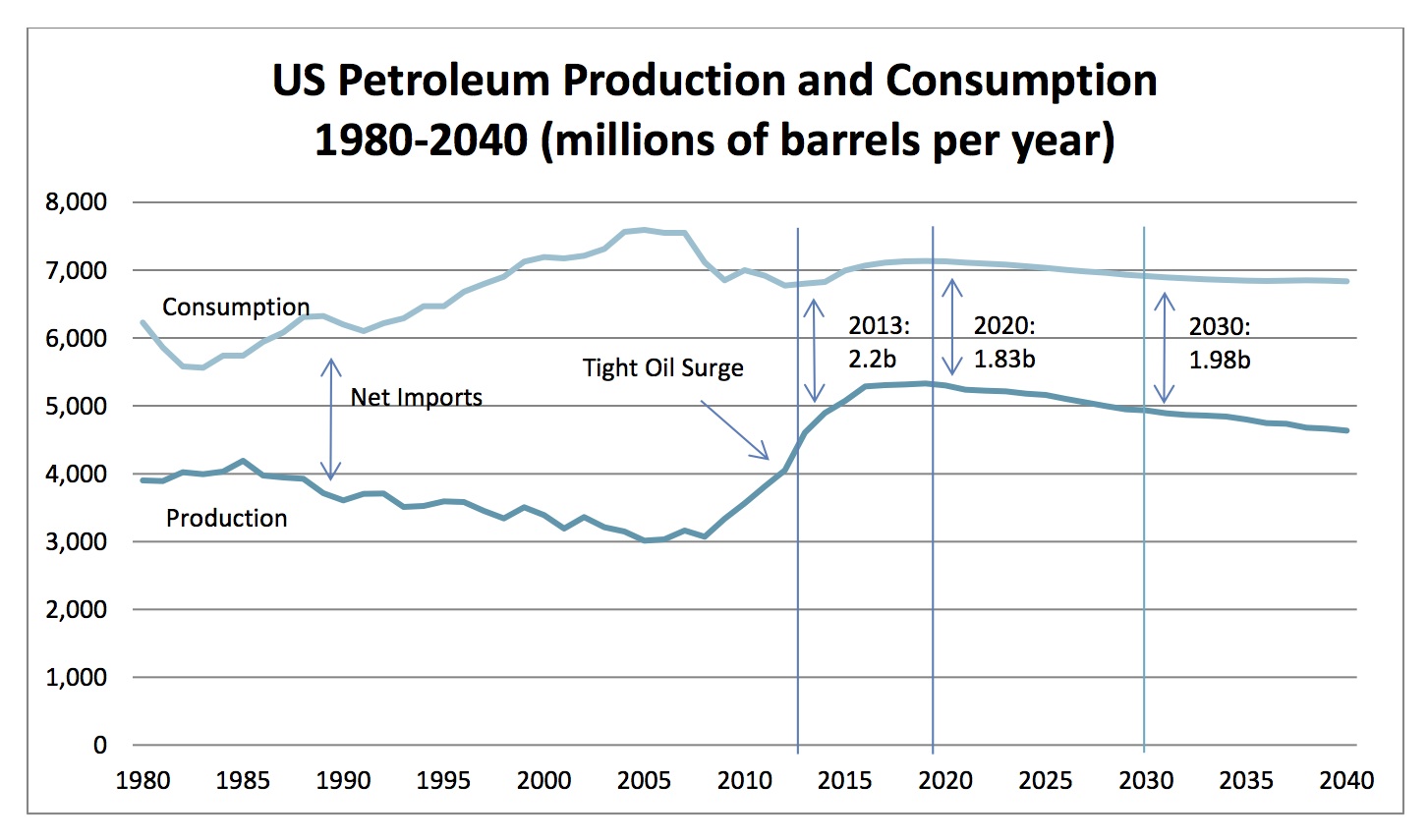

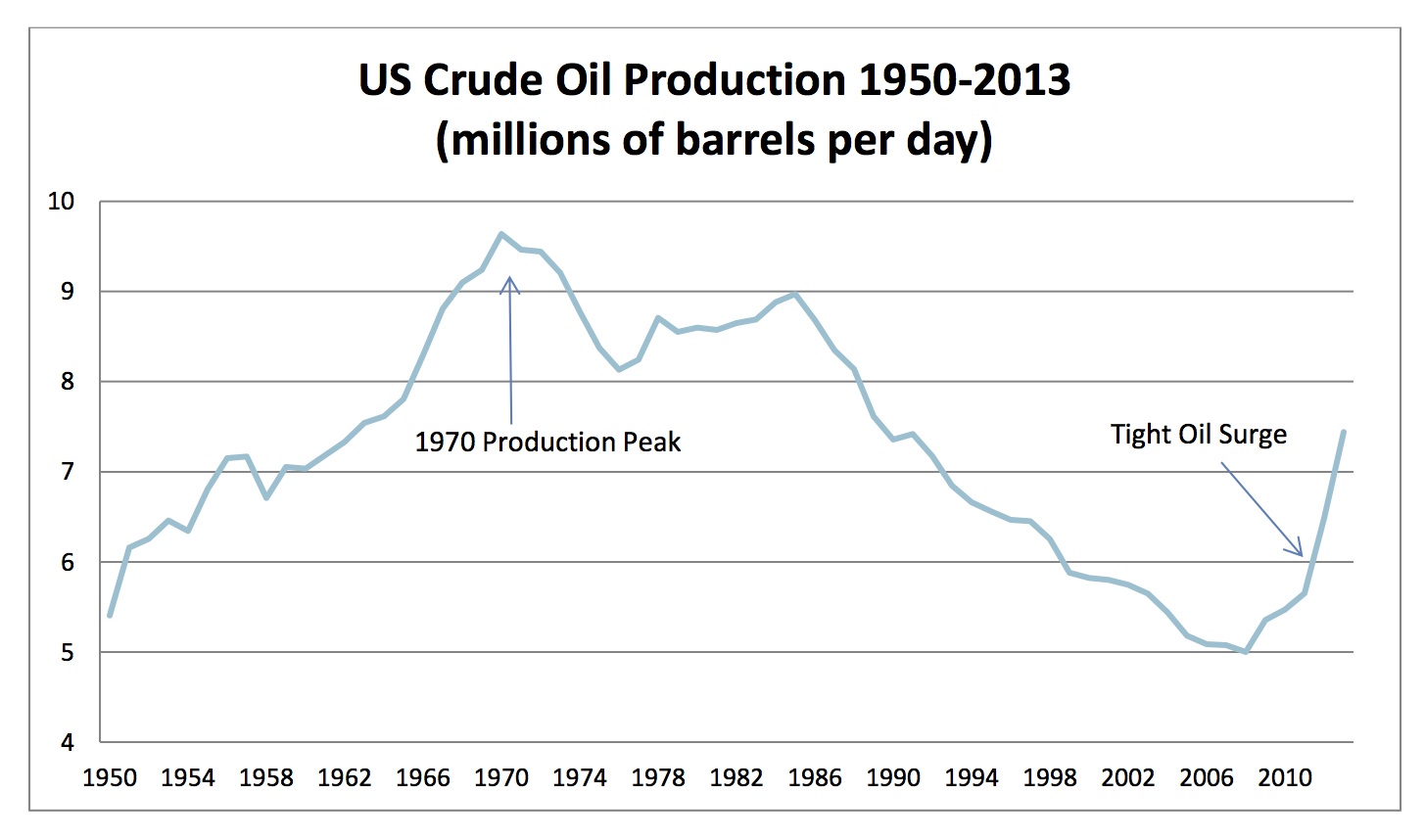

It is this figure which is often cited as the most significant and disparaging regarding American efforts to achieve energy independence. While significant petroleum reserves exist within the United States, most of them are expensive and difficult to recover. Most of those reserves which are economical are already in operation and have been in production decline since the early 1970s. It is true that the recent expansion of hydraulic fracturing and horizontal drilling techniques have reversed this trend for the past few years, but most observers agree that tapping “tight” oil formations will provide only a brief reduction in the rate of decline for American domestic oil production before the most profitable wells are depleted and the surge normalizes.

This long-term stagnation in domestic petroleum production has been particularly problematic because of the reliance of the US transportation sector on oil. Whereas coal or natural gas can be burnt in place of petroleum to power turbines in electric power plants, and wind farms, solar farms, dams, and nuclear plants can provide electricity to the US power grid, the American automotive fleet does not enjoy so much diversity. Alternatives to gasoline engines do exist, but have consistently failed to make significant headway into the mass consumer market. Even with more advanced and efficient electric cars being developed, petroleum still accounts for over 92% of all transportation energy to the less than 1% electric vehicles claim, with the difference being made up by ethanol biofuels and natural gas vehicles.

There are a number of reasons for this, first and foremost being that petroleum is a very efficient fuel source in terms of energy output per gallon, as well as cheap to extract from the ground and easy to ship overseas. If the United States is to achieve energy independence, however, it must reduce or replace its petroleum consumption (overwhelmingly in vehicles) or find and extract petroleum from American oilfields to satisfy existing demand without importing foreign oil. This is no small task, as every day the US imports 9.8 million barrels of crude oil to keep its economy running.

Despite this, there is still cause for optimism. Even with only moderate gains in domestic petroleum production expected over the long term, American demand for petroleum has been decreasing steadily since 2003. This is largely due to improvements in the fuel efficiency of cars, the increasing price of gasoline at the pump, and the 2008 economic recession. Average gasoline prices reached a peak in 2008 and, while dropping from that year until 2010, have remained above $3.00 per gallon in the years since. Those American consumers who responded to changing market incentives and purchased more efficient vehicles or travelled fewer miles per year are now affecting a reduction in petroleum demand even as production has increased.

Even so, a growing US population makes it very unlikely that the US will cease importing petroleum under current conditions even in the long term. The Energy Information Administration’s (EIA) forecasts assume that even past the year 2040, the US will still need to import one third of its petroleum barring any policy changes that increase production at home during that time. Since nearly all energy that America imports is in the form of petroleum, removing the need to import it is central to a successful energy independence strategy.

Reducing Petroleum and Natural Gas Imports

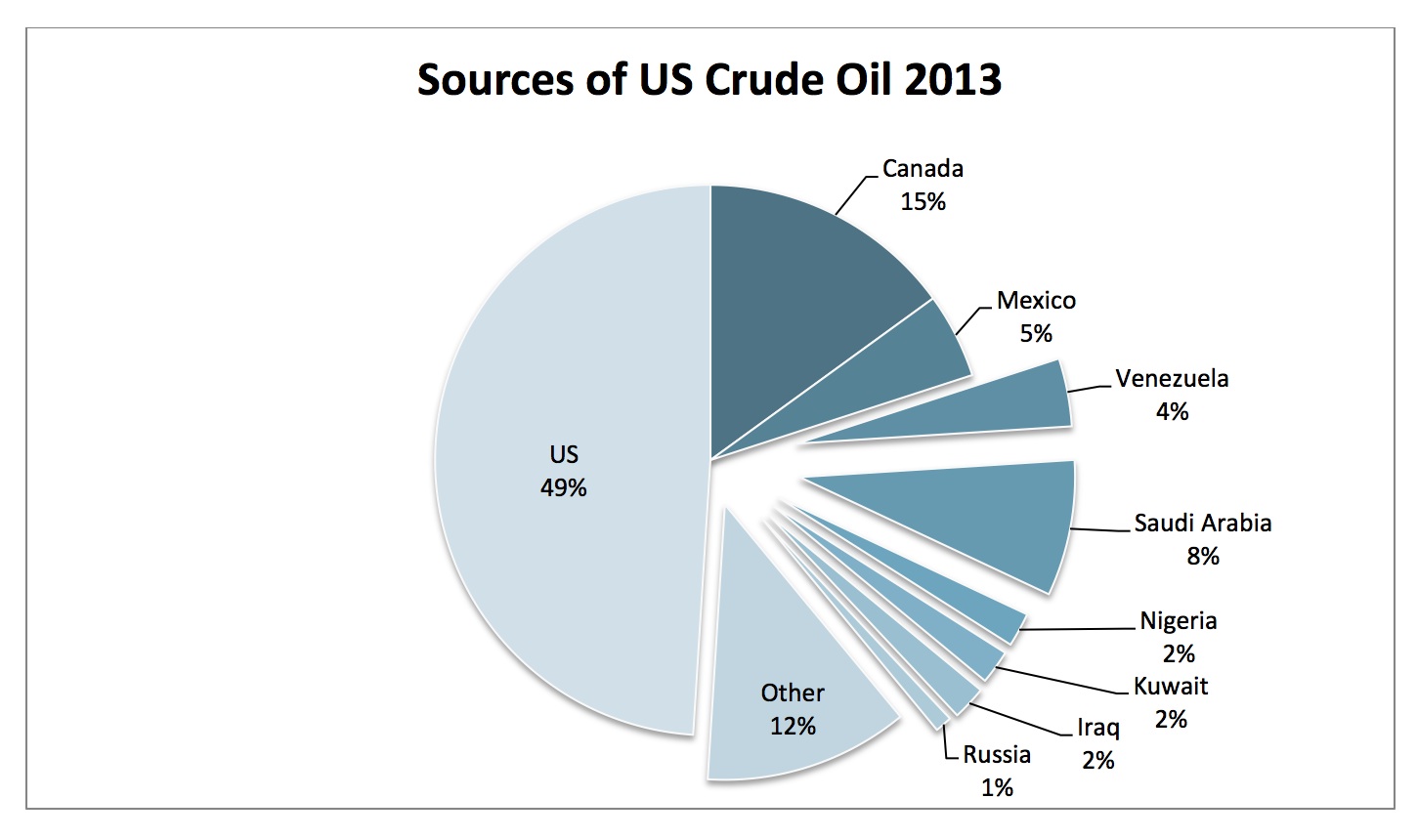

Every year, the United States consumes 6.75 billion barrels of petroleum products. As previously mentioned, decreasing per capita demand and rising efficiency standards are slowing the rate at which this number grows annually, but by 2030 a larger economy and higher population will increase demand by at least 4% to 7 billion barrels per year according to EIA estimates. In 2013, the US produced just over 4 billion barrels of petroleum at home, satisfying about 60% of this demand. The remaining 2.73 billion barrels represent total petroleum imports. Of these, 1.65 billion originated from the OPEC nations and Russia, the countries Americans are primarily wary of relying upon for energy security. It is these 1.65 billion barrels of petroleum which this analysis focuses on most, as even if American energy independence proves infeasible, North American energy independence may not be and reliance on OPEC could still be reduced or eliminated.

Canada and Mexico are key trade partners of the United States, and most Americans are far more comfortable importing their energy needs from these two neighboring nations than from the rest of the world. In 2013, Canada and Mexico exported a combined 1.08 billion barrels to the US, meaning that they represented roughly 49% of all petroleum imports. So, if American, Canadian, and Mexican production were to collectively increase by 1.65 billion barrels annually, North America would achieve energy self-sufficiency and the United States would no longer be compelled to import energy from OPEC and Russia.

Reducing overall petroleum imports to diminish reliance on exporters outside of North America could be accomplished by:

• Encouraging the expansion of shale gas production to remove the need to import foreign natural gas;

• Encouraging the expansion of tight oil production, closely linked to shale gas production;

• Opening untapped domestic petroleum reserves on the Alaskan North Slope;

• Opening the Arctic and Gulf outer continental shelf (OCS) to petroleum exploration and production;

• Expanding infrastructure necessary to increase imports of petroleum from the Canadian oil sands;

• Preparing for a reduction of Mexican petroleum imports as Mexican proven reserves are depleted;

• Incentivizing the replacement of vehicles with alternative energy variants; and

• Increasing the share of biofuels such as ethanol in the energy budget to replace petroleum.

Expansion of Shale Gas Production

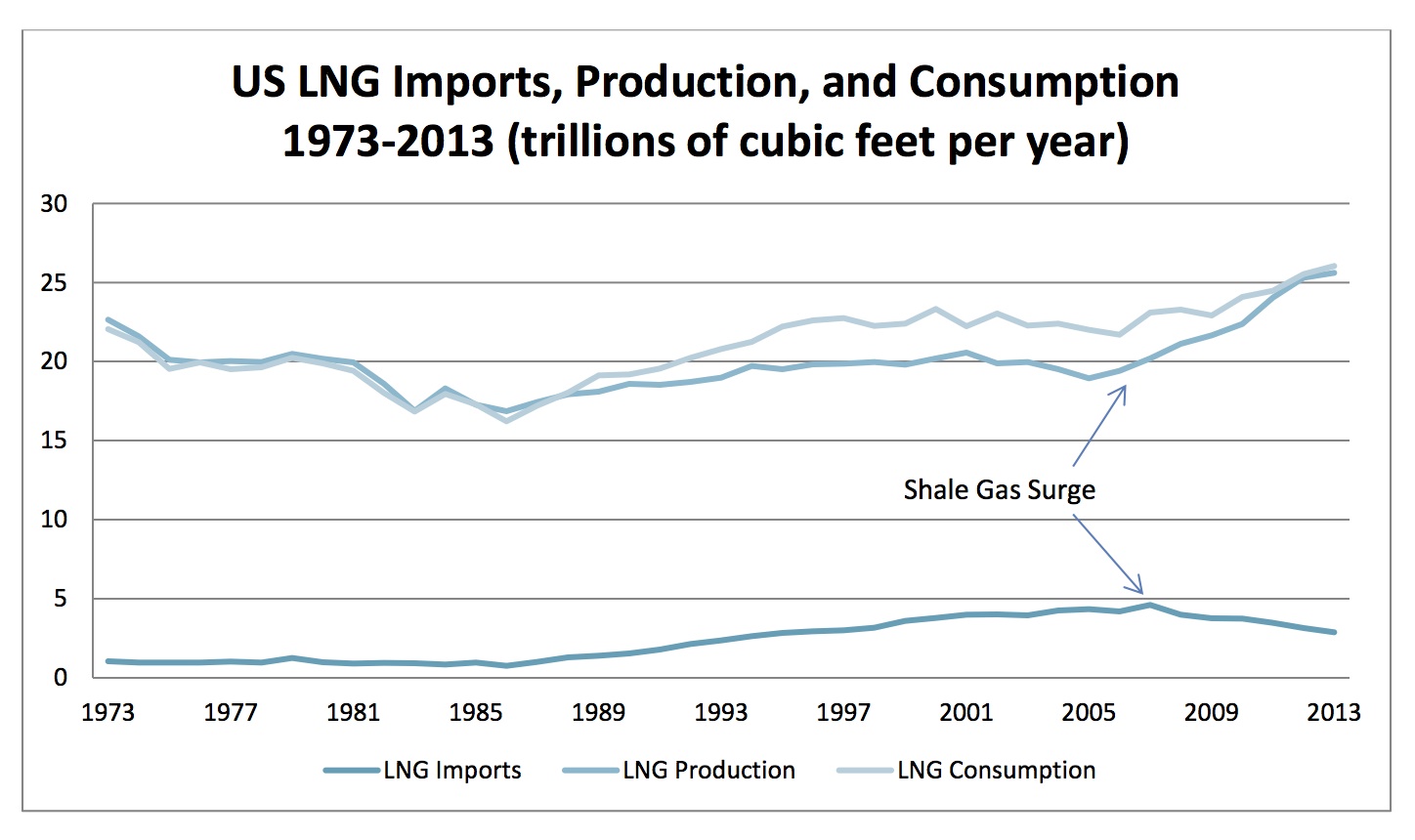

Liquefied natural gas (LNG) accounts for about 14% of energy imports (about 2% of all US energy consumed). Historically, American imports of LNG have increased rapidly as the fuel found numerous applications in industry, home heating, cooking fuels, and as an alternative for coal and petroleum in electric power plants. Total imports of LNG climbed from 1 trillion cubic feet (tcf) every year in 1986 until peaking at 4.5 tcf in 2007.

The advent of hydraulic fracturing, or “fracking”, as a technique for more efficiently and economically removing natural gas reserves trapped in dense shale rock formations has reversed this trend. Over the past six years, imports of foreign natural gas have fallen to under 3 tcf – less than the US imported in 1997. As domestic production increased, so too has domestic consumption as a glut of cheaper natural gas displaces coal as a source of energy in electricity generation.

North America’s geology features immense shale formations, or “plays”, from which this shale gas is being mined. The largest of these formations are the Marcellus play, which lies beneath the states of New York, Pennsylvania, and West Virginia, the Haynesville play, which straddles the Texas-Louisiana border, and the Barnett play in north-central Texas. The three together account for an estimated 70% of proven recoverable shale gas reserves, amounting to 530 tcf. Given that the rate of US natural gas consumption stands at roughly 27 tcf per year, this means that there is nearly two decades’ worth of natural gas contained in these formations alone, with more proven reserves being discovered every year. Advances in technology and industrial practices or evolving market conditions may expand this number as time goes on, with some projections venturing as much as a 100 year supply of natural gas being locked in shale.

This rapid expansion of natural gas production is most likely to plateau over the next few years as the most profitable wells dry up and are replaced with less profitable ones. Even with a normalization of the natural gas surge, however, the estimated size of recoverable reserves is large enough to credibly assume very competitive domestic natural gas prices for several decades. So long as these trends continue, and most data seems to confirm that they will, the US can expect to be more than self-sufficient in natural gas. The primary concern for realizing complete energy independence, then, is petroleum.

Expansion of Tight Oil Production

The same shale gas reserves currently being recovered through hydraulic fracturing techniques also frequently contain petroleum, which is found trapped with natural gas inside impermeable shale formations. This “tight” oil can only be pumped to the surface if it coexists with significant amounts of natural gas, which carries it through the fractures created during drilling through the borehole and to the surface. The surge in shale gas production has therefore also yielded a closely-linked surge in tight oil production, the success of which has reversed the overall decline of US domestic oil output and allowed it to reach levels not seen since 1964.

At 53 billion barrels, the United States possesses the second-largest estimated reserves of tight oil in the world, though there is much dispute over how much of these reserves are proven economically recoverable. Also, while production increases have been dramatic for the past seven years and probably will continue to be so for the next ten to twelve, most experts believe that production levels will thereafter plateau as the most profitable and most-easily accessed reserves are drained and less economical ones take their places. Regardless, tight oil production is forecasted by the EIA to continuously provide domestic petroleum at sustainable averages which would have been dismissed even 10 years ago. Given that there is no short or even medium-term substitute for crude oil, used so overwhelmingly by American vehicles in transportation, it is vital that tight oil production continue if the goal of energy independence is to be met.

Alaskan North Slope and ANWR Oilfields

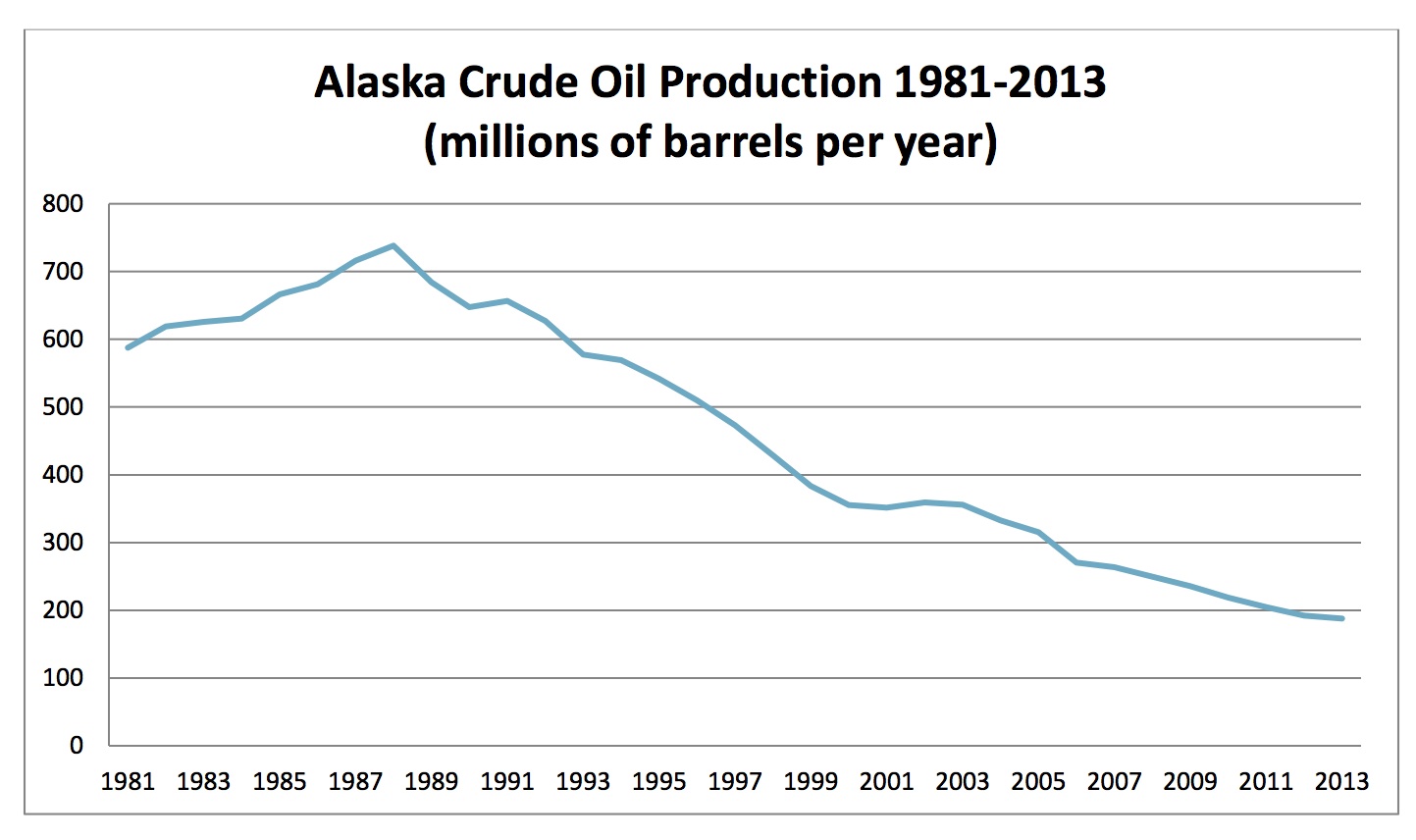

Aside from tight oil, there are other light oil reserves which could be exploited by the United States to increase domestic production, most notably those in Alaska. Oil has been drilled in the Alaskan North Slope since 1977, though all fields currently in operation have peaked and are now in production decline. The state of Alaska’s total production currently sits at about 200,000 barrels of crude oil per year and is expected to produce gradually diminishing amounts over the next decade.

However, the untapped oilfields beneath both the Alaskan National Wildlife Refuge (ANWR) are believed to contain an additional eight billion barrels of oil, making them some of the largest oilfields in the United States. Exploration of these fields has been restricted due to the protected status of the territory as a wildlife reserve, but studies conducted by the EIA in 2008 confirmed the eight billion barrel figure and concluded that it would take at least 10 years from approval until full production could begin in ANWR should the legislative ban be lifted. If exploration were to begin this year, returns would not be seen until 2023 and highest production yields are estimated to be realized 10 years following that, placing peak production in 2033. At that point, with modern technology, the ANWR field could produce up to 287 million barrels of crude oil per year (800,000 barrels per day), a 59% increase over current state production.

Arctic, Californian, and Eastern Gulf OCS

The final significant untapped reserve of petroleum in North America lies on the outer continental shelf (OCS), the submerged landmass of North America that extends several hundred miles from the coastline before dropping off the continental slope to the ocean floor. An estimated 86 million barrels of petroleum reserves are believed to exist on the OCS, 70 billion of which are economically recoverable under current oil prices. Of these, over 63 billion (90%) lie either in the Gulf of Mexico or off the northern coastline of Alaska.

The recent expiration of restrictions on exploration in this area has led to the discovery of several new oilfields there and raised interest amongst prospectors in the neighboring Eastern Gulf Coast OCS zone adjacent Florida which remains off-limits by executive order until 2022 at the earliest. Plans by the Obama administration to rescind this order and open the Eastern Gulf of Mexico for exploration and drilling were scheduled to come into effect in 2010, but were promptly cancelled after the Deepwater Horizon oil spill that same year. The State of Florida has similarly banned exploration and drilling for oil in its own waters, which extend about 10 miles out to sea before entering federal jurisdiction. Even if these bans were lifted, there is little information about the potential reserves the Eastern Gulf OCS may hold. Exploratory wells dug as far back as the 1960’s yielded poor results, as did international ventures across the Florida Strait in Cuban waters. Regardless, the American Energy Alliance (AEA) estimates that up to 3.4 billion barrels of commercially exploitable oil may exist there, which could be tapped for production in as few as five to seven years.

The state of California also holds large potential reserves of offshore petroleum, estimated at 6 to 7 billion barrels by the Minerals Management Service (MMS) and over 10 billion by the AEA. As in the Eastern Gulf OCS region, exploration and leasing of the OCS within state waters has been banned by the state government and deadlocked politically in federal waters. Production on these sites could begin in as few as five years, and some even sooner as existing platforms (which predate the leasing bans) could access known deposits immediately.

The MMS has also estimated that as much as 19 billion barrels of proven oil reserves are located on the Alaskan OCS adjacent to the North Slope in the Chukchi and Beaufort Seas. Shell Oil has worked for years to secure the necessary permits and approvals to explore and drill these fields, though the process has been plagued by numerous delays. Should current targets for 2015 exploration be reached, however, the Department of Energy (DoE) has released models for what hypothetical production of these fields would look like. Though Arctic offshore drilling is more expensive per barrel than onshore drilling, experts remain confident that both Arctic fields could economically produce a mean estimate of 1 million barrels per day between them (365 million barrels per year). As with the ANWR field, this peak production number is not expected to be attained until 20 years after the start of operations, placing it between the years 2034-2036. If production in the Gulf of Mexico and California were of similar efficiency, an estimated 100 million barrels per year could be added to this sum, for a total of at least 450 million barrels per year being drawn from the American OCS.

Expansion of Canadian Oil Sands Import Capacity

If production in the United States is insufficient to remove the need to import petroleum, then the next best option would be to import as much as possible from Canada instead of the Middle East, Africa, and South America. Canada is currently America’s leading source of energy imports, and has great potential to become an even larger trade partner in the future thanks to their own plentiful reserves. While stopping short of true energy independence, the US would at least be able to remove dependency on more unstable and less accommodating regions of the world for its energy by finding it in North America.

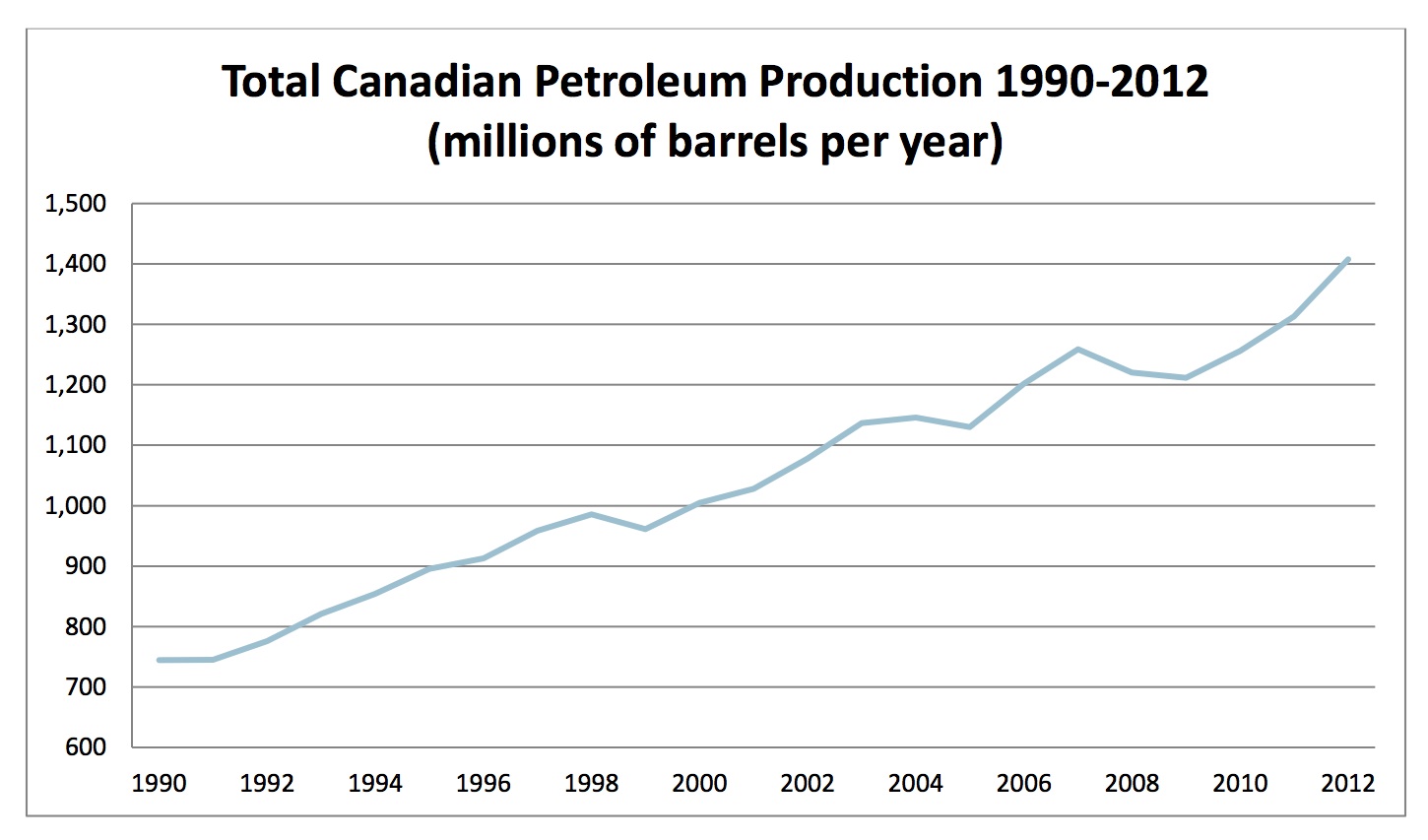

The Athabasca oil sands of Alberta, Canada, with over 1.17 trillion barrels of technically recoverable reserves, represent the third largest concentration of petroleum in the world after Venezuela and Saudi Arabia. These hydrocarbons are composed primarily of heavy crude-laden sediment called bitumen, which is much thicker and more difficult to extract and refine than either Saudi or Venezuelan oil. Despite this increased cot, consistently high energy prices over the past 10 years and proximity to the world’s largest petroleum importer have made these reserves economical, and mining operations have been extracting and transporting bitumen across the US-Canadian border by rail and pipeline in ever-increasing amounts. Nearly all of the recorded growth in Canadian oil production for the past decade is attributed to these deposits, and the long-term global demand for more energy ensures that this growth will continue at a rapid pace.

By 2020, the oil sands are expected to almost double their production from 0.6 to 1.17 billion barrels per year. Total Canadian oil production will as a result increase about 50% by this point, from 1.16 to 1.79 billion barrels per year. By 2030, mined bitumen is expected to account for over 85% of all crude production in Canada, which will have doubled 2005 figures for a total of 2.2 billion barrels per year. Of this, over 1.9 billion barrels could be exported to the United States.

Despite this impressive growth potential, the geographical location of the oil sands complicates access to the American market. Overland transportation is far more expensive per mile and per ton than transportation by ship, and therefore moving the bitumen from Canada by rail deeper into the US interior accrues significant costs and limits the range at which it can be economically sold. The construction of cost-saving pipelines is therefore crucial to Canadian suppliers which want to sell energy resources to American customers farther from Alberta. The Keystone XL pipeline, which is the most famous and politically divisive of these projects, would enable Albertan oil to be economically transported as far as the American south and still remain competitive with African, Middle Eastern, and Venezuelan oil arriving by tanker. If pipeline capacity to the US were not increased, Canadian suppliers are likely to build pipelines to Vancouver so that oil sands crude could be sold overseas, probably to energy-hungry Asian markets. This would prevent the expanded oil production in Canada from helping the United States reduce its imports from outside North America, and forestall the achievement of North American energy independence.

Diminishing Mexican Imports

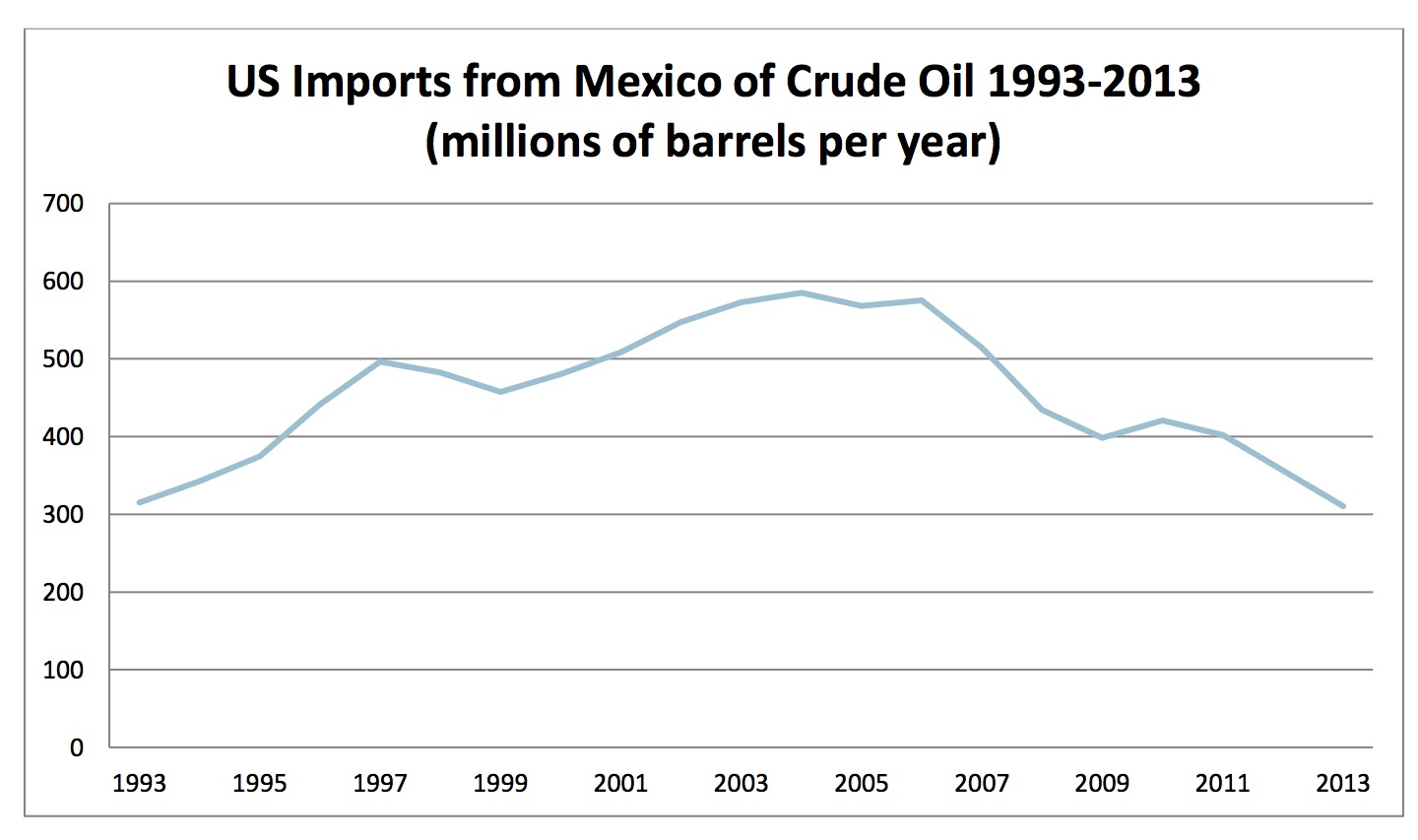

Mexico, like Canada, is a longtime and well-trusted trading partner of the United States which has supplied it with energy for decades. In contrast to Canadian production and its impressive expansion, however, Mexico’s oil production has stalled and rapidly declined since 2004. This is largely due to the gradual depletion of the supergiant Cantarell offshore oilfield which has provided most of Mexico’s production for the past 30 years and for which there is no known replacement of similar magnitude within Mexican territory. The government of Mexico has estimated that it only possesses 13 billion remaining barrels of technically recoverable crude oil, most of which is spread between smaller fields which are difficult to access or costly to operate.

These problems are further compounded by Mexican regulations which have restricted PEMEX, Mexico’s state- owned petroleum export company, from courting foreign investment to assist in tapping these deposits. Efforts are underway by the current administration to end this restriction, but even if more advanced drilling techniques were introduced Mexican oil production is slated to decline for the foreseeable future. Given this pessimistic outlook for the future of Mexican petroleum exports, by 2030 the United States should expect to import only about 100 million of the 300 million barrels per year it currently receives from Mexico.

Transition to More Efficient Vehicles

While expanding domestic production of petroleum has the potential to increase the supply of gasoline to the US transportation sector, a transition of motorists to newer and more fuel-efficient vehicle alternatives would reduce demand for the same resource. Policymakers are realistically incapable of enacting a shift from one type of vehicle to another without dramatically imposing on the liberties of consumer choice, but policies and financial incentives can be structured in a fashion that accelerates their adaptation and makes them more attractive to consumers. Tax credits and subsides, for example, have been used to encourage the sales of more energy efficient vehicles for years.

A large spectrum of alternative energy vehicles exists, but they can be easily classified into three categories: electric vehicles (EVs), natural gas vehicles (NGVs), and hybrid engine vehicles (HEVs). Each has its own selection of advantages and disadvantages regarding petroleum consumption compared to traditional internal combustion (IC) engines, and its own challenges finding traction in the American auto market.

Electric Vehicles (EVs)

Electric vehicles under current technology constraints do not reduce total energy consumption, but by drawing energy from the US power grid instead of from liquid fuels they do shift consumption from petroleum to other domestically-available energy sources such as coal, natural gas, and nuclear power. Because they require zero fossil fuels to function, EVs uniquely allow renewable energy sources to be harnessed in the transportation sector, enabling them to contribute to a reduction of energy imports. However, EVs suffer from three major drawbacks which have discouraged Americans from purchasing them over conventional gasoline-powered ones: price, range, and infrastructure.

Regarding price, EV batteries and propulsion systems are very expensive compared to internal combustion engines, and rely on expensive rare earth metals such as cobalt and lithium for the efficiency necessary to hold electrical charges over extended periods of time. Most of these rare earths are imported, as South America, Asia, Africa, and Australia possess reserves far in excess of North America’s. As a result, even if a massive transition to EVs was made, the United States would still be reliant on the imports of a rare resource for the production of the batteries, effectively changing the foreign dependence from fuel to rare materials. Expensive rare earths also inflate battery costs which are carried over to the consumer, placing them well over the price range of most buyers and making them economically uncompetitive with IC engines. Ford’s all-electric model of the Focus, for example, features a battery which costs an estimated $15,000 alone, which is nearly triple the production cost of a similarly-sized IC engine. And while electric vehicles do reduce operating costs for the owner over time by removing the need to refuel with expensive gasoline, studies conducted by the Congressional Budget Office have concluded that over the lifetime of an electric vehicle, an owner will pay over $12,000 more than he would for a traditional vehicle. While efforts are being made by automakers to reduce this cost, electric models are not anticipated to become competitively affordable for the medium term, except for those wealthy buyers which can afford the additional costs.

Regarding range, most EV batteries are also currently incapable of holding enough power to give a vehicle more than an 80 mile range before its charge is depleted. For Americans who live in urban centers, this isn’t a major problem. Unfortunately, American cities and road systems have been designed under the assumption of readily- available gasoline engines that enable people to travel hundreds of miles without refueling. Suburban and rural residential areas are sufficiently far from commercial areas to make EVs impractical for many commuters, who have for the past century been steadily leaving cities for suburban communities. Larger, more advanced batteries with greater ranges do exist, but at exponentially higher costs.

Finally, even in those urban centers in which range is of less consequence to commuters, the lack of public charging centers remains an obstacle to many prospective EV owners. An estimated 30% of all vehicles in most cities are parked curbside overnight, and unless massive construction projects were undertaken by urban centers to make access to the power grid available to these vehicles, they could not be recharged during idle periods. Homeowners with garages would be able to install their own charging stations for their personal use, but high property values in urban centers will price those buyers which can’t afford garages out of this option. The installation of public charging centers or the upgrading of public and private parking garages could address this, but the large investment costs are too daunting given the current small size of the EV market.

Natural Gas Vehicles (NGVs)

Vehicles powered by natural gas offer another alternative to internal combustion and electric vehicles. Other nations such as Argentina and Iran have sizable NGV fleets which have demonstrated the technology on large scales, even amongst commuters and personal light vehicles. Though natural gas-powered engines replace petroleum with either compressed natural gas or liquefied natural gas, they continue to benefit from many of the same conveniences liquid petroleum does, making them a simpler replacement alternative than EVs.

Foremost, natural gas offers a range efficiency middle ground between petroleum and electric batteries. While a typical modern gasoline engine delivers over 300 miles of range per tank in a midsized car, a natural gas vehicle promises only 200 miles. This isn’t because natural gas is a less-efficient fuel – in fact, a gallon-equivalent of natural gas is about a third more efficient than petroleum – but rather because the systems required to store natural gas in either a compressed form or as a super-cooled liquid are far larger than those required to store petroleum, which remains liquid at all normal temperatures of operation. NGVs which are designed to use the same highway space and carry the same number of passengers are therefore incapable of carrying as much fuel as an IC vehicle of the same class. Even with its inferiority to petroleum in this regard, natural gas engines still far outperform electric vehicles, most models of which offer less than 100 miles of range per charge.

The current low price of domestic natural gas offers another reason to seriously consider incentivizing the purchase of NGVs. The ongoing boom in domestic shale gas production has driven down the cost of natural gas dramatically, making it very competitive with petroleum in many capacities. At the time of writing, natural gas prices were just under half the price of petroleum per BTU. And while increased demand for this fuel would drive up prices should more motorists switch to them, most credible estimates project at least 75 years of reserves being available within the United States even at increased rates of consumption.

Despite these advantages, NGVs still suffer from many of the same obstacles that EVs do: range, price, and infrastructure. While a given NGV does offer longer ranges than a comparable electric vehicle, many motorists are still uncomfortable with a vehicle that must be refueled 33% more often. Also similar to EVs, NGVs cost a significant margin more than IC vehicles. Fuel savings require years of use to begin to recoup the additional expense at purchase, and most American auto buyers don’t have the available income to make such an investment. Finally, natural gas refueling stations are sparse, even more so than electric charging stations. Until larger numbers of drivers begin using the vehicles, there is little incentive for them to be built, and so long as they aren’t built, there is less incentive for new auto buyers to purchase them.

Companies and services which travel predetermined routes and stop frequently for servicing, however, make excellent candidates for replacement since installing their requisite refueling and maintenance infrastructure would be far simpler. Larger vehicles such as buses and trucks for which size is not a concern have made attractive options for NGV conversions, and some US bus systems and trucking fleets have already integrated them into their fleets to reduce fuel costs. Though NGV variants of trucks are more expensive per unit by as much as $5,000-$10,000, the low price of fuel and the high mileage these vehicles accrue on a daily basis would see that extra expense repaid and converted to savings within just two years of operation. Many US fleets have already begun investing in these vehicles under the Clean Fleets Partnership or outside of it.

Hybrid Engine Vehicles (HEVs)

Hybrid engines are a combination of internal combustion and electric-charge propulsion systems which alternates between the two modes to increase fuel economy. These variants of alternative energy vehicles are by far the most popular amongst American consumers, with over 3 million having been sold compared to only 200,000 plug-in EVs and 275,000 NGVs. HEVs enjoy numerous unique advantages which have made them the most successful improved-efficiency variant on the American market.

First, hybrid engines still use petroleum as their source of propulsion, with the electric drive train being used to extend mileage. This means that they do not require the use of specialized refueling centers but still significantly reduce petroleum consumption per mile driven. HEVs are therefore an excellent transition vehicle because existing petroleum infrastructure can be used as more efficient models and better pure electric alternatives become available, permitting a more gradual transition from gasoline refueling to electric recharging. Plug-in hybrid models exist, but where charging stations cannot be reliably found non-plug-in models remain an easy consumer choice.

Also, despite using electric batteries as EVs do, HEVs mitigate range concerns by switching to conventional gasoline or diesel once battery charge is depleted, making the vehicles more suitable to American geography and suburban/rural layouts. They do not require significant change in the driving behavior of American motorists, making them easier choices for consumers which are hesitant to make such an expensive investment in a vehicle that has unfamiliar demands attached to it. They are also the least expensive of the three alternatives, making them available to a wider number of auto buyers.

HEVs are, however, alike other IC replacements in that they remain more expensive. A hybrid vehicle costs between 18-25% more than an IC vehicle of the same class, and with the expiration of government tax credits on hybrid vehicles (they only remain on plug-in models), this price figure remains a major obstacle for mid and low income earners at the time of the vehicle’s purchase. Even with increased fuel efficiency, most hybrids will not recover their costs until at least 10 years of use.

Federal Incentive Policies for Fuel-Efficient Vehicles

The federal government has enacted a number of policies aimed at making each of these high fuel economy vehicles more affordable to encourage them to be adopted in greater numbers. The most significant of these is the federal tax credit offered to those who buy a new alternative energy vehicle, which for most variants amounts to $7,500. The Congressional Budget Office has determined that this tax credit has succeeded in increasing the sales of new EVs, HEVs, and plug-in hybrid electric vehicles (PHEVs), but they have not reduced the amount of gasoline consumed every year on the road.

This counterintuitive observation is explained by the interaction of the tax credit with the Corporate Average Fuel Economy (CAFE) standards imposed on US automakers. All vehicle manufacturers are required to sell a selection of vehicles every year which, once averaged, falls beneath a maximum emissions and fuel consumption limit set by the government. Federal tax credits given to consumers have allowed manufacturers to sell more EV and HEV models per year than they otherwise could have, but only because federal tax revenue artificially reduces the prices of these vehicles and not because of increases in efficiency or reductions in the cost of production. Once these vehicles are sold, the average fuel economy of their products increases and the manufacturer is enabled to sell a greater quantity of less-efficient vehicles for competitive cost, resulting in negligible net gains in fuel efficiency that will cost taxpayers a total of $7.5 billion by 2019. In an effort to raise average fuel efficiency, then, tax credits have polarized auto sales into two fuel efficiency extremes.

Advocates of the tax credits argue that while it is true they have indirectly contributed to putting less fuel efficient vehicles on the market, they have also successfully increased the number of high efficiency vehicles being driven by Americans today. Because the price of installing EV- and PHEV-compatible infrastructure is determined in large part by the number of the vehicles in use, a greater number of them on the roads would lower production and infrastructure costs and facilitate a faster transition to a higher fuel economy transportation sector in the long term.

Reforming the CAFE standards to require production quotas of certain vehicles variants instead of enforcing economy averages may also achieve more desirable results, but the higher cost of these vehicles would be carried by the American consumer and would therefore result in less vehicles being sold. This would affect a contraction of economic activity, both as fewer vehicles were made and purchased and as the workforce became less mobile. Higher tax credits could help offset this cost, but only if they were increased to over $12,000 per vehicle – a sum which would be drawn from federal taxes, which would merely transfer the source of the economic cost from the vehicle’s higher price tag to higher tax rates every year.

Increasing the Use of Biofuels

Petroleum use in vehicles can also be reduced by blending or replacing them with biofuels, which are fuels created through the fermentation of biomass into combustible products. Sugarcane is the most efficient source of fuel in terms of energy output per ton of harvest biomass, but ethanol produced from corn remains the only significant source of biofuel in the United States due to North America’s drier climate. Because corn is a replenishable resource, it has the potential to become a sustainable source of long-term energy which is already compatible with vehicles of modern manufacture. This means that, in theory, petroleum could be replaced by ethanol if only the capacity to produce it on commercial scales was large enough. While there is no consensus amongst the scientific community about exactly how energy efficient ethanol really is compared to fossil fuels, most agree that it is a significant source of net energy despite the energy inputs of labor, harvest, and transport associated with its production.

There are numerous other concerns about expanding the use of ethanol as a fuel, however, foremost being the actual economic efficiency of such a dramatic shift in fuel sources. Ethanol, while deceptively cheaper per gallon at the pump, only yields about 65-75% the mileage per gallon as traditional gasoline, meaning more of it is required for the same energy output. Once this is accounted for, ethanol is actually 22% more expensive than gasoline, and therefore amounts to an effective tax on motorists who must fuel their vehicles more often. Expanded production and larger economies of scale may address this is the future, but at present only massive government subsidies and federal mandates have allowed ethanol to remain a competitive source of fuel.

The corn required to make ethanol also requires the use of large amounts of farmland. On average, 11 acres of farmland are needed to fuel one typical car for one year in the United States. Even at current levels with most gasoline containing only 10% ethanol, 40% of American corn cropland has been allocated to ethanol production. Suitable agricultural land is finite, and if more were needed to create ethanol for fuel purposes other crops would be pushed out to accommodate corn planting, or prices on other food items would rise as farmland became more expensive. Altogether, unless dramatic advances in productivity are made to get more ethanol from the same acreage, further promoting it as a petroleum replacement may result in a significant loss of wealth and economic activity.

Anticipated Effects of Energy Independence

What benefits the United States could expect to see should it attain energy independence is a topic of much debate. Proponents often cite reduced energy prices, a reduction in America’s trade deficit with the rest of the world, additional jobs, and a more stable supply of energy as economic incentives for pursuing an aggressive independence strategy. More security-related benefits advocates hope to achieve are reducing the market share and influence of OPEC member nations and various “petrodictatorships” which rely on energy exports for revenue, as well as alleviating the pressure to diplomatically and militarily stabilize conflict-prone regions which currently provide petroleum to the US economy. Unfortunately, many of these promised benefits have been overstated, though a few offer genuinely significant prospects.

Negligible Effects on Energy Prices

Oil prices are a factor of a global market which is much larger than the total US share of it. As such, attaining energy self-sufficiency would mean very little for the average American consumer who pays for petroleum, as even impressive gains in domestic petroleum production would be diluted by the size of the total world petroleum output. Barring mercantilist tariffs, fluctuations in the price of oil abroad will still affect oil process domestically so long as American and Canadian oil producers have access to foreign consuming economies. The resource will be sold the highest available bidder, and Americans will therefore have to bid more in times of high demand or low supply.

To illustrate this, consider a political event in the Middle East which could lead to a sudden shortfall in oil production there: a conflict between Iran and Saudi Arabia. Such as outbreak would lead to dramatically reduced oil exports from both nations as the Straits of Hormuz were blockaded or shipping was threatened by either. Even if the United States imported none of its oil from the either country, supplies to Europe and Asia would both be reduced and prices in both regions would therefore increase. Canadian petroleum producers in the Albertan oil sands region or even American producers along the gulf coast would then be able to make higher profits by shipping their crude across either ocean to satisfy demand in China and Europe, where the commodity is scarcer and therefore more expensive. This would lead to decreased supply in the US, as oil which once found its way from North American fields would be diverted to foreign markets, forcing domestic prices to rise in tandem with those abroad until equilibrium was reached. In sum, increased domestic supply of oil would do little to nothing to insulate the US from global price shifts.

Reduced Trade Deficit

The hypothetical Middle Eastern conflict described above illustrated how energy independence for the United States or North America would not reduce oil prices or protect them from disaster-induced shifts. One significant development in the above scenario, however, is that if global petroleum supplies were threatened and prices rose suddenly, the producers which made higher profits per barrel sold would be American or Canadian instead of Middle Eastern. This means little to the average consumer in either nation who would still pay more at the pump to fill their vehicle, but it would reduce the impact such an event would have on national GDP. Wealth would still be lost as economic activity across all sectors slowed, but more of the global energy market would be represented by American or Canadian firms which would actually make considerable profits assuming no changes in their own production.

How beneficial this would be to an American not employed by the oil industry is much-debated, as the value of corporate reinvestment in the domestic economy is difficult to measure. Even so, the most conservative estimates of gains are still better than the transfer wealth overseas. If energy independence were to occur naturally, without the aid of government funds drawn from taxes or market-distorting regulations, then a growth of oil and other energy profits at home would reflect increased American competitiveness in the field and true wealth generation, not reallocation at the collective expense of the population. Increased corporate profits would be taxed to provide revenue to the federal government, as well, and could be used to fund federal initiatives or to reduce the national debt.

More difficult to measure but no less important are the trade skills, expertise, and familiarity with technological practices participation in an industry provide to the American population. Such trade skills are a key contributor to the productivity of the workforce, and a revitalized domestic petroleum industry would potentially increase the number of laborers with exposure to them, amounting to an investment in future economic potential. So even with only modest immediate employment gains relative to the size of the American population, there are significant benefits to promoting the growth of any domestic technical industry. In a time of ever-increasing international competition, a well-skilled and versatile labor force cannot be underestimated.

Increased Supply Stability

While achieving energy self-reliance would have marginal effects on energy prices, it would have a positive effect on the reliability of that energy reaching the marketplace. The US Strategic Petroleum Reserve was created as a buffer for sudden drops in supply to mitigate shortages and normalize their effect on the US economy. Having access to more stable supplies of petroleum would accomplish the same goal. While American and Canadian petroleum would become more expensive during a supply disruption, it would almost certainly be available for sale at higher prices.

Even without this assurance, the chances of OPEC successfully orchestrating an oil embargo such as that inflicted on the US in 1973 is small. Geopolitics have evolved in such a manner that Saudi Arabia, concerned by the increasing influence of its regional rival Iran, has more closely aligned itself with the US. Additionally, the long- term effect of the 1973 embargo was the sudden and dramatic interest generated in securing alternative energy sources and reducing petroleum consumption per capita, both of which have manifested impressive changes in the trends of energy usage among Western nations. Inciting another such revolt against petroleum could negatively impact the economic prospects of oil exporting states, most of which rely on hydrocarbons for the majority of their government revenues and GDP growth. Saudi Arabia has often communicated its intentions to meet supply demands for the world to promote global stability and disincentivize a global transition away from fossil fuels, their chief export commodity.

Modest Benefits for Employment

There is no clear answer how many jobs would be created if domestic oil resources were tapped in the United States. The US petroleum industry currently employs about 2.4 million people. Far more are employed in jobs which are tangentially related to the oil industry, though what qualifies an oil-dependent job is a difficult question to answer and varies immensely depending on the criteria chosen to define it. Generous figures which include airline crew members who rely on low jet fuel prices and service staff that serve oil industry employees inflate this figure to nearly 10 million jobs, even though there is no consensus on how many of these jobs would be lost should the US oil industry enter recession.

Likewise, construction projects associated with petroleum infrastructure offer deceptive statistics. While thousands of jobs will be created to complete the construction of the Keystone XL pipeline, for example, less than 50 of these jobs would remain after the pipeline was completed. Such infrastructure projects are designed to employ as few people as possible to reduce upkeep costs and maximize profitability, and therefore offer very few long-term benefits in term of employment to the US labor force. More long-term jobs such as those connected to drilling, refinement, and production are better indicators of actual job growth. A typical oil well can remain active for as long as 30-40 years under the proper conditions, and require both lower skilled and more technically-demanding labor to continue operating. These employees require an expanded services sector near there workplace, further accelerating economic activity in the regions the growth occurs.

Reduced Market Share and Income of Petrodictatorships and OPEC States

Any increase in global energy supply would intuitively lead to a decrease in prices, even if that decrease were very marginal. However, the global market for petroleum as it currently exists does not resemble a true free- market and therefore does not behave as such. The member states of OPEC, which control over 80% of the world’s proven conventional oil reserves, collude to orchestrate oil production and exports between themselves irrespective of competitive market forces. In this way OPEC resembles a cartel, which is similar to a monopoly except that production is controlled by a small number of actors instead of a single actor. As is typical of both monopolies and cartels, OPEC carefully controls the output of all of its members’ production through the imposition of quotas in order to keep oil prices artificially high and maximize the profitability of that resource for the producers.

An expansion of production in non-OPEC states such as the US and Canada would place considerable pressures on OPEC’s decision-making. If Albertan oil sands production reached 4 million barrels per day and consequently reduced the American demand for Venezuelan oil, the increased supply would constrain OPEC’s leadership to reduce their own production by a similar 4 million barrels per day in order to keep prices at their preferred levels. While this prevents savings from being passed on to American or Canadian consumers at home, it does reduce the income of OPEC states abroad, which now sell less petroleum than they did prior to the rise in Canadian production. The wealth is then effectively transferred from OPEC states to non-OPEC states, even if most of this doesn’t provide direct or immediate benefits to the consumers in either.

Even with this consideration, rapidly growing demand for energy in Asia assures that OPEC states will have no difficulty selling their oil resources. Total global demand for petroleum is expected to increase 50% over the next 20 years, so the creation of an oil glut and a collapse in oil prices such as was seen in the 1980s is highly unlikely. Even with an expansion of North American petroleum production, far more rapidly expanding demand in Asia will mitigate most of the effects of a comparatively smaller market share for OPEC, who would have no trouble finding other buyers. That being said, even if global demand is set to rise, every barrel of oil produced in North America represents one which is not produced by petrodictatorships or OPEC. Even if Iranian or Russian oil revenues were slated to increase, the rate at which they did would be adversely impacted by a self-sufficient United States or North America. Considering the dominant shares of revenues petroleum and natural gas represent in these nations, even a minor shift of this nature is not to be dismissed lightly.

Uncertain Implications for American Security Commitments Abroad

Given that a reduction in demand for foreign energy (particularly petroleum) would have little effect on the ultimate price of that energy at home, it is uncertain if there would be a decreased incentive for the US to continue protecting the stability of global energy flows. Energy security would continue to be negatively impacted by regional instability in the Middle East, Africa, and South America regardless of a 100% self-sufficient energy economy in North America, doing little to alleviate the compulsion of the United States to enforce stability in expensive military endeavors or through the bolstering of allies with military aid. Even should the US supply of energy be insulated from sudden shocks, production falls in the Middle East or Russia would inflate prices in North America and lead to severe shortages in Europe and Asia.

Disruption of these foreign economies would have a deleterious effect on the US economy, especially in those sectors which rely most heavily on international trade. Those products which are created through the use of foreign energy and then exported to the US would inflate in price, carrying the economic costs through “indirect energy imports.” The motives behind US security interests in volatile regions of the world, then, would not disappear even if the sources of its energy changed.

Conclusions

Even after the great gains in petroleum production precipitated by the ongoing tight oil surge in the US, the feasibility of achieving US energy independence by 2030 hinges on its ability to reduce petroleum imports by two billion barrels per year by that time. The two most promising sources of domestic petroleum which could be tapped to eliminate these imports are the ANWR oilfield of Alaska’s North Slope and various petroleum reserves located on the US outer continental shelf.

The OCS of Alaska holds the most promise for additional long-term growth at 365 million barrels per year. The Gulf of Mexico OCS could potentially yield a further 100 million barrels per year, and the estimated reserves beneath ANWR could produce 287 million more. Totaled together, this amounts to 752 million barrels of petroleum per year by 2030 if exploration in all three locations were to begin today, which is only 38% of the production required to satisfy demand by the target year. Domestic production alone will therefore be insufficient to satisfy the expected level of demand, even with the advancement of stricter fuel economy standards on American vehicles.

However, 40% of current crude oil imports come from Canada and Mexico, both of which are close trading partners of the United States. If Canadian exports increase proportionally with anticipated production increases, by 2030 nearly 2 billion barrels annually consumed in the United States could come from Canada alone, a 95% increase over current levels. Even with pessimistic estimates from Mexico anticipating a production decrease of 200 million barrels per year by 2030, a net gain of 900 million barrels per year over current levels is possible between the two.

This means that while American energy independence seems out of reach, North American energy independence is not. The massive production gains expected in Canada combined with the output from Mexico and US domestic reserves could total 2.75 billion barrels per year by 2030. This figure exceeds expected US petroleum consumption by such a wide margin that even if the US were not to open any of its Alaskan or OCS reserves to production, it would still have no need to import petroleum from anywhere outside of North America. This is only possible if increased volumes of Canadian petroleum can reach more distant US markets for competitive cost. To that end, pipeline projects such as Keystone XL are vital to any strategy of displacing oil imports from outside North America. Without them, Canadian oil will remain uncompetitive with foreign oil arriving by tanker, and even dramatic increases in Canadian production figures would not result in a reduced dependence on OPEC for most regions of the United States.

The conversion of a larger percentage of the American auto fleet could also significantly reduce petroleum consumption, but the far higher prices of every available alternative to the traditional combustion engine makes them poor choices for the vast majority of American customers. Federal tax credits and other incentives which have attempted to make these vehicles more attractive have thus far failed to affect an increase in the overall efficiency of the American auto fleet, largely because they have permitted auto manufacturers to sell larger numbers of less efficient vehicles alongside EV and HEV alternatives. A continuation of these policies may eventually reduce the high costs of infrastructure construction and conversion as more alternative energy vehicles entered circulation, but such savings are impossible to measure and come at the cost of billions of tax dollars and reduced economic activity. Their compatibility with existing fueling infrastructure make hybrid vehicles the most promising transition vehicle, though even they are still too expensive to be expected to rapidly replace conventional vehicles without much larger federal tax credits. So, with the exception of large public and private fleets such as trucking, bussing, and delivery services, improved fuel economy vehicles cannot be counted on to significantly reduce petroleum consumption for some time.

Finally, even if North American energy independence were achieved, the benefits would be modest. Economic benefits include a reduction of the trade deficit by $60-75 billion per year if domestic reserves were tapped, and there would be intangible benefits to productivity which exposure to industrial trade skills would provide the American workforce. Prices of gasoline would be minimally impacted, and new jobs created for more than a few years are more likely to number in the thousands than in the millions. Energy supplies would be less volatile, but would still be adversely impacted by flare-ups in other energy-exporting regions as international market prices were driven upwards.

Because of this, US policymakers would still have strong incentives for promoting stability in the Middle East, even if doing so carried high economic and military costs. Failing to keep the global energy market stable would result in global economic shocks that would eventually carry over to the US economy whether its energy came directly from those regions or not. From a strategic perspective, however, a reduced reliance on OPEC petroleum would compel the cartel to reduce their production quotas and adversely affect their revenues, which many OPEC states are heavily dependent upon.

. . . . . . . . . . . . . . .

Kenneth Bloomquist writes on matters of foreign policy, national security and energy and was invited by Frontiers of Freedom to prepare this study and analysis of US energy outlooks.