The End of Free-Lunch Economics

Smart economic policymaking invariably requires trading off some pain today for greater future gains. But this is a difficult proposition politically, especially in democracies. It is always easier for elected…

Smart economic policymaking invariably requires trading off some pain today for greater future gains. But this is a difficult proposition politically, especially in democracies. It is always easier for elected…

U.S. Senator Rand Paul (R-KY) recently introduced his own “Three Penny Plan” federal budget that will balance within five years by assuming the repeal of the Bipartisan Budget Act of…

“After the phony cliff, we face the terrifying one.” by Conrad Black Last week, Fareed Zakaria and Charles Krauthammer appeared in Toronto (where I live much of the time), and…

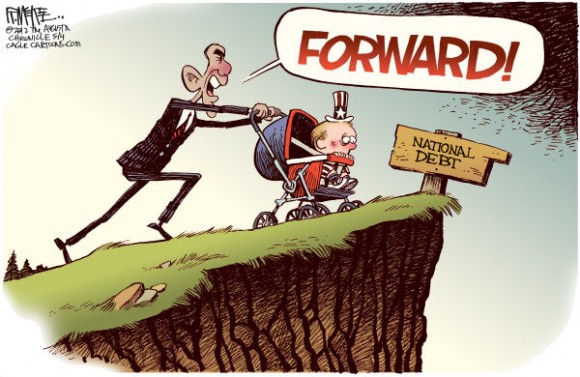

by George Landrith President Barack Obama repeatedly chided Mitt Romney’s budget plan during the presidential campaign on at least two grounds: (1) it lacked detail, and (2) the math didn’t…