The Dangers of Endless Quantitative Easing

Inflation readings in the United States have shot up in recent months. Labor markets are extremely tight. In one recent survey, 46% of small-business owners said they could not find workers…

Inflation readings in the United States have shot up in recent months. Labor markets are extremely tight. In one recent survey, 46% of small-business owners said they could not find workers…

by Peter Morici • FoxNews The U.S. economy created only 142,000 jobs in August, down from 212,000 in July, indicating the economy significantly slowed this summer. Job creation…

by Ralph R. Reiland I think the poor need another Reagan in the White House. The income of black heads-of-households dropped by 10.9 percent from June 2009 to June 2013.…

How do you know the August jobs report was pretty bad? When the best thing you can say is that it might have met Wall Street expectations if not…

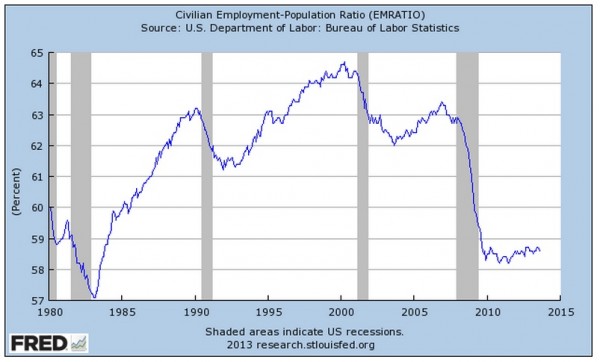

The “labor force participation rate” hit a record low hit at 63.2 percent. This represents the percentage of Americans over the age of 16 who have jobs (even if it is part-time or…

The left and “progressives” love to blame wage stagnation on greedy businesses wanting to gobble a larger share of the pie. But it’s actually a product of businesses’ uncertainty about…